McMillion Financial Group

your partner in retirement planning

your partner in retirement planning

| |

| |

| |

| |

| |

| |

The Power of Tax-Deferred Compounding

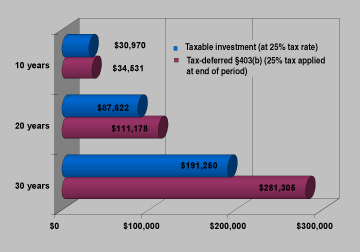

In this hypothetical illustration, we'll analyze the scenario for a monthly contribution of $250 into a

403(b) plan that is earning 8% APR versus the same monthly contribution and earnings rate in a

taxable investment with a 25% tax rate.

This hypothetical example is not intended to illustrate the performance of an actual investment.

This illustration is not an indication or guarantee of future performance. The illustration is a

hypothetical analysis that is calculated using a single compounded rate of return, which is highly

unlikely as rates will vary over time, particularly for long-term investment fees or expenses, which

would lower performance.

A taxpayer saving in a taxable investment would first have to pay tax on the $250 earmarked for

saving, netting only $187.50 for deposit each month. In 10 years, the taxable investment would

have grown to $30,970 while the 403(b) investment would be at $34,531, net after taxes--a

difference of $3,561.

The difference is that in the taxable investment, taxes were paid on all of the gains thus reducing

the amount saved. With the 403(b) plan, the entire investment was permitted to grow tax-deferred.

Over a period of 30 years, the difference is even more dramatic. Here the taxable investment

grows to just $191,250 while the tax-deferred investment grows to $281,306 net after taxes. The

difference is a whopping $90,055!

All the funds that were paid out from the taxable investment to cover the taxes were allowed to

remain in the tax-deferred 403(b) investment to compound over all those years. With a 403(b)

account, those funds were working for the investor throughout that entire period of time. And

while 403(b) assets are subject to taxes upon withdrawal, investors often find themselves in a

lower tax bracket at retirement than when they were working. This means the amount paid in

taxes should be less.

In this hypothetical illustration, we'll analyze the scenario for a monthly contribution of $250 into a

403(b) plan that is earning 8% APR versus the same monthly contribution and earnings rate in a

taxable investment with a 25% tax rate.

This hypothetical example is not intended to illustrate the performance of an actual investment.

This illustration is not an indication or guarantee of future performance. The illustration is a

hypothetical analysis that is calculated using a single compounded rate of return, which is highly

unlikely as rates will vary over time, particularly for long-term investment fees or expenses, which

would lower performance.

A taxpayer saving in a taxable investment would first have to pay tax on the $250 earmarked for

saving, netting only $187.50 for deposit each month. In 10 years, the taxable investment would

have grown to $30,970 while the 403(b) investment would be at $34,531, net after taxes--a

difference of $3,561.

The difference is that in the taxable investment, taxes were paid on all of the gains thus reducing

the amount saved. With the 403(b) plan, the entire investment was permitted to grow tax-deferred.

Over a period of 30 years, the difference is even more dramatic. Here the taxable investment

grows to just $191,250 while the tax-deferred investment grows to $281,306 net after taxes. The

difference is a whopping $90,055!

All the funds that were paid out from the taxable investment to cover the taxes were allowed to

remain in the tax-deferred 403(b) investment to compound over all those years. With a 403(b)

account, those funds were working for the investor throughout that entire period of time. And

while 403(b) assets are subject to taxes upon withdrawal, investors often find themselves in a

lower tax bracket at retirement than when they were working. This means the amount paid in

taxes should be less.

Securities offered through Fortune Financial Services Corporation. member FINRA and SIPC

_______________________________________________________________________________

Copyright 2006 McMillion Financial Group LLC. All rights reserved. Revised July 12, 2019.

______________________________________________________________________________

_______________________________________________________________________________

Copyright 2006 McMillion Financial Group LLC. All rights reserved. Revised July 12, 2019.

______________________________________________________________________________

Branch Office: 111 2nd Ave NE, Suite 913B, St. Petersburg FL 33701

Phone: (727) 456-1518 E-mail: kmcmillion@mcmillionfinancialgroup.com

McMillion Financial Group LLC is not an affiliate of Fortune Financial Services

Inc.

Phone: (727) 456-1518 E-mail: kmcmillion@mcmillionfinancialgroup.com

McMillion Financial Group LLC is not an affiliate of Fortune Financial Services

Inc.